An RRSP is not meant to be a short term or temporary investment. However, you may withdraw all or part of your investment at any time*. RRSP withdrawals are subject to tax and the terms of the investment in the plan. Withholding taxes apply on funds withdrawn from an RRSP except when the funds are being transferred from one RRSP top another, or when being transferred into a Registered Retirement Income Fund (RRIF).

*There are withdrawal restrictions that will apply to locked-in RRSP plans.

There are two scenarios that permit you to withdraw funds from your RRSP without incurring income tax: buying a qualifying homer or going back to school. The Home Buyers Plan (HBP) allows you to withdraw up to $25,000 from your RRSP investment for the purchase of a qualifying home. The amount you withdraw must be repaid (replaced in your investment) within 15 years; subject to a minimum annual repayment that is 1/15th of the amount withdrawn.

If you are going back to school, the Lifelong Learning Plan (LLP) allows you to withdraw up to $20,000 from your RRSP investment to pay for eligible training or education for you, your spouse or your common law partner. Once you withdraw the funds, you have 10 years to repay the money.

When you are ready to start withdrawing funds from you RRSP investment, or by the end of the year in which you turn 71 (whichever comes first), you must convert your RRSP into a Registered Retirement Income Fund (RRIF). With a RRIF, your investment can continue to grow on a tax-deferred basis but you are required to withdrawal at least a minimum amount each year. You may choose to increase the amount or the frequency you receive funds from your investment, as long as the minimum is withdrawn. (Please note, locked-in plans have specific restrictions, please contact one of our Investment Specialists to learn more).

If you simply withdraw the money from your RRSP investment, you will have to pay the withholding tax on it and the money withdrawn will be classified as income for you in that taxation year. Depending on your income level, you may still be required to pay income tax on this amount on top of what was already paid with the withholding tax.

While you can contribute to your RRSPs at any time during the year, you only have 60 days into the New Year; until March 1st (or February 29th during a leap year); to have the deposit be deducted from your income for the prior tax year, current year or future year(s). Once this date has passed, any contributions made can be applied to the current year’s income (or subsequent year’s income).

You are able to contribute each year up to December 31st in the year in which you turn 71. After that date, you may not make further deposits to your RRSP and it must be withdrawn or converted in to a RRIF.

(Please note: when the deadline falls on a weekend, the Canada Revenue Agency (CRA) may extend the deadline to the following Monday).

After filing your taxes last year, you received a Notice of Assessment from the Canada Revenue Agency (CRA), stating your maximum contribution for the current year. To get your contribution room, visit the CRA’s website by clicking here, or call their TIPS hotline at 1-800-267-6999.

The amount you are allowed to contribute is determined by the “earned income” you report on your tax return. It is 18% of your previous year’s “earned income”, up to an annual limit. Each year, the annual limit set by the government changes. To find out the limit for this year, please visit the CRA Website.

This limit may be reduced if you belong to a pension or deferred profit sharing plan through your employer (refer to your T4 slip). It can also be increased if you do not contribute the full allowable amount in the previous year or years.

If you go over the limit, you are penalized 1% a month on the excess amount. Although, up to $2,000 may be over-contributed during your lifetime without penalty. To be safe, it is always better to check with CRA or your Notice of Assessment to confirm your annual contribution limit.

If you do not make your maximum annual RRSP contribution, any unused portion is automatically brought forward, so you can use it in future year(s).

Any Canadian up until the age of 71 who earns income and/or still has contribution room available may contribute to an RRSP. Even if you are not taxable, you should file a tax return to report your earned income and create RRSP contribution room.

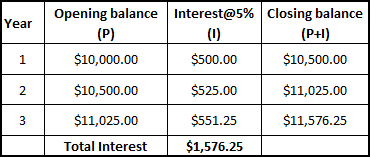

Compound interest (or compounding interest) is interest calculated on the initial principal and also on the accumulated interest of previous periods of a deposit or loan. It means, over the course of your investment, you will earn interest on the interest you have earned in previous years, as well as on the principal deposited. This causes the investment to grow much faster.