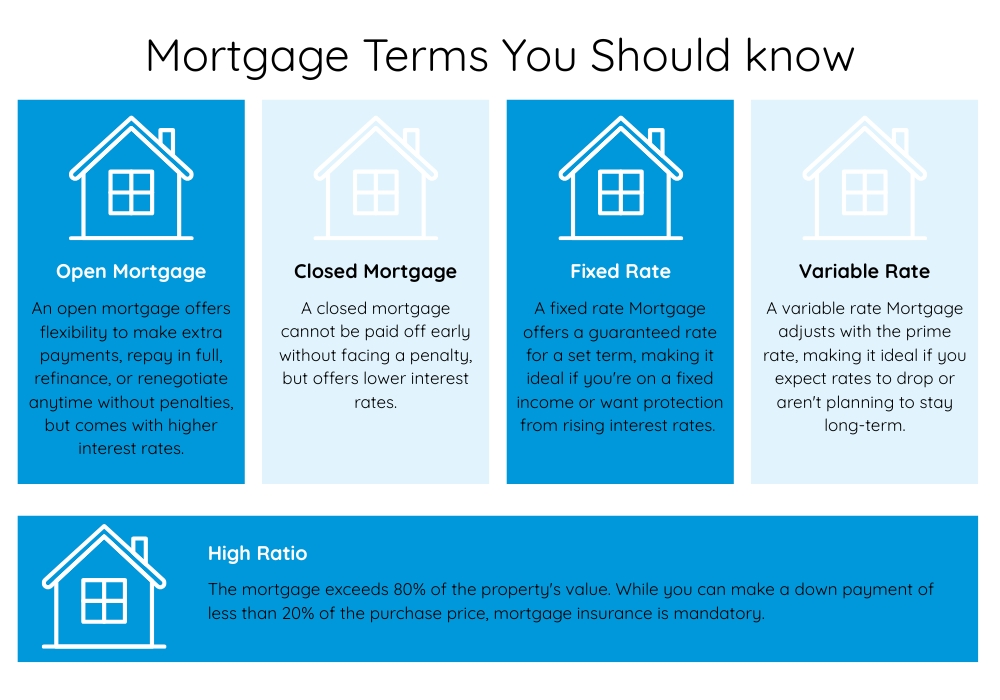

Whether you’re buying a home, renewing your mortgage, or planning a renovation, Kingston Community Credit Union will help tailor your mortgage to suit your needs.

4.45%

4.65%

4.60%

Ready to buy your first home? KCCU is here to help make the process easy and stress-free. Through CMHC, we can assist you in qualifying with as little as 5% down.

CMHC (Canada Mortgage and Housing Corporation) is a crown corporation of the government of Canada. Their web site can guide you through the process of determining what you need in order to qualify for a mortgage as a first-time homebuyer.

A KCCU Lending Specialist is here to guide you every step of the way. Book an appointment today and get expert advice on all your home-related questions.

Thinking of upsizing to your dream home, downsizing to something more manageable, buying a rental property or perhaps a cottage?

Let our experts guide you through the process.

Thinking about a new kitchen, a fresh coat of paint, or a total makeover? Now’s the time!

Let’s bring your vision to life.

Your dream home starts with a vision and KCCU will help bring it to life with expert guidance and financing tailored to your needs.

Time for a change?

Make the move to KCCU and experience the credit union lending difference!

Take advantage of the equity you have built in your home with a low-interest Home Equity Line of Credit.

From renovations to that dream vacation or perhaps just combining other debts, a home equity line provides you with the funding and flexibility you want.

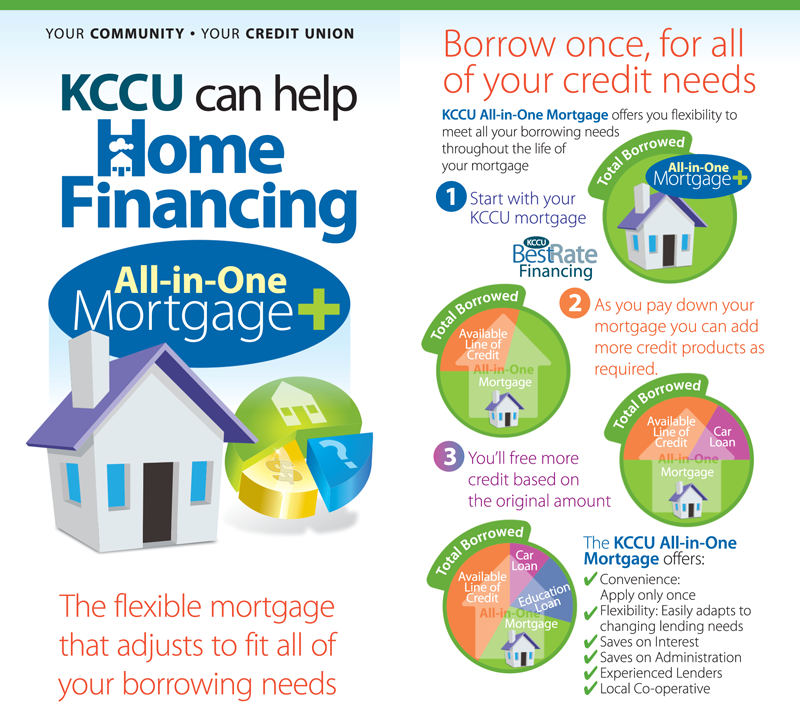

The KCCU All-in-One Mortgage offers you flexibility to meet all your borrowing needs throughout the life of your mortgage.

As you pay down your mortgage you can increase the limit on the Home Equity Line of Credit portion or even add more credit products up to the original approved limit.

Be prepared for future home improvements or repairs as you need them with more credit made available based on the amount paid down on your mortgage.

Going green at home helps the environment and saves you money.

Whether it’s better insulation or energy-saving upgrades, a KCCU Green Home Loan or Line of Credit can help you get there. Learn More.

With mortgage protection, you can protect your family financially for less than you think.

Creditor’s group insurance is optional and is underwritten by Co-operators Life Insurance Company. Supporting services, such as enrolment intake, medical underwriting and claims administration, are provided by the employees of CUMIS Services Incorporated, a subsidiary of Co-operators Life Insurance Company. Coverage is governed by the terms and conditions of the creditor group insurance policy issued to the creditor and is subject to terms, conditions, exclusions, and eligibility requirements. See the Product Guide and Certificate of Insurance for full coverage details. To contact CUMIS, A Division of Cooperators Life Insurance Company, visit www.cumis.com or call 1-800-263-9120.

A third party is an individual or entity, other than the account holder or those authorized to give instructions about the account, who directs what happens with the account. For example, if an account were opened in one individual’s name for deposits that are directed by someone else, the other person or entity would be a third party.

{kind=link}